Financial institutions employ a variety of terms to distinguish between various aspects of their operations. Let us examine two of them: the available balance and the ledger balance. These terms may be unfamiliar to you, but the difference between ledger balance and available balance is critical.

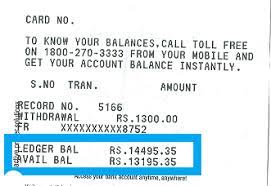

What is Ledger Balance?

A bank computes a ledger balance at the end of each business day. It incorporates all withdrawals and deposits to determine the total amount of money in a bank account. The ledger balance is the opening amount in the bank account the following morning. It remains constant throughout the day.

After all transactions have been approved and executed, the ledger balance is updated at the end of the business day. Banks compute this amount after recording all transactions. It includes deposits, interest revenue, wire transfers that go both in and out, and cleared checks. It indicates the account balance at the start of the next business day.

A ledger balance example might help you grasp the definition. For example, suppose you start your week with a $500 starting checking account balance. Then receive a $1,000 paycheck deposit and make a $200 debit on your bank card. Despite these additional transactions, your ledger balance on Monday will be $500 for the whole day. This is due to the fact that the check has not yet cleared. The debit transaction is still outstanding, and your ledger balance is based on the beginning of the business.

Can you spend your ledger balance?

No, you should not rely on the ledger balance to track your spending. Transactions may not always clear promptly, the ledger balance may be higher or lower than the accessible balance.

What is Available Balance?

The available balance is the current amount of a checking or savings account, less any outstanding payments and deposits. It subtracts the entire amount of all processed and posted credits and debits from the total amount of any outstanding payments that have yet to be fully processed. This results in a more accurate picture of the money in your account that is still available to spend.

Any financial activity will quickly modify the available amount. Therefore, every time the account holder does a transaction, the available balance changes.

Banks calculate available balances in two ways:

- Your ledger balance plus or minus any debits or credits up to the time you check your balance.

- Your ledger balance minus any unprocessed deposits or checks.

Ledger Balance vs. Available Balance

This distinction is significant since you should typically only make payments based on the amount in your ledger balance. The ledger balance is the actual amount. But the available balance is the prospective amount after all unprocessed transactions are completed.

Ledger balance varies from the customer’s available balance, which is the total amount of money available for withdrawal. The ledger balance does not reflect real-time transaction updates. It stays constant throughout the day. The available balance fluctuates throughout the day as transactions post to the bank account. Neither balance includes outstanding checks made from the account. But the available balance is updated when information about recent ATM withdrawals and other transactions is received by the bank.

Let’s imagine you make a $500 payment from your bank account at 12 p.m. Then you access your net banking account to check your account balance. However, you notice that your ledger balance is $5,000, whereas your available balance is $4,500. What is the source of the imbalance? The ledger balance represents the balance of your account at the start of the day. As a result, the $500 payment you made at 12 p.m. will not be reflected. It shows a $5,000 balance, which you had at the start of the day. Your available balance, on the other hand, displays the current balance of your account. As a result, it will take the $500 payment into account and then display your balance.

Similarly, any checks placed into your account during the day will not be included in your ledger balance. You will only see the difference after your bank gets the money from the deposits into your account.

Difference between Ledger Balance and Available Balance

| Ledger Balance | Available Balance |

| The account balance at the conclusion of a business day is represented by the ledger balance. | The total amount that an account holder can remove from their bank account is referred to as the available balance. |

| You cannot always access your Ledger Balance. | You may check your available balance at any moment. |

| When you take money from your account, it is instantly deducted from the ledger balance. | When you take money from your account, it is subtracted from your available balance only once the money is debited from your account. |

| Any transactions that are not completed will not be shown in the ledger balance. | Any transaction, complete or unfinished, will affect the available balance. |

How to calculate ledger balance?

- You may compute your ledger balance by starting with the opening balance, subtracting any debits, and then adding any credits/deposits.

- Debits can be any transaction done during the day, such as a bank card transaction. Credits involve both deposits, such as wages, and payments or refunds from consumers.

- You may calculate your current ledger balance by adding the credits and subtracting the debits from your opening balance.

How long does it take the ledger balance to be available?

The ledger balance is frequently changed to reflect the available amount. The ledger balance is usually accessible within less than 24 hours. A bank processes a record balance at the end of each business day. It includes all withdrawals and deposits to determine the total amount of money in a ledger. The record balance is the ledger’s starting equilibrium the next morning. It continues as before day in and day out. Thus, the ledger balance may take up to 24 hours to clear. Ledger balances are processed at the end of the business day.

Leave a Reply